The stock I’m talking about today is LVMH (Louis Vuitton Moët Hennessy) which I guess needs no introduction. It's a brand that is easily recognizable and counts Lisa and Zendaya, to name a few A-listed celebrities who endorses their brands. But does being a world class brand translate into a compelling stock to invest in?

Please note this is not a buy or sell recommendation and do your own self diligence when investing.

1. Company Overview

LVMH was created in 1987 through the merger of fashion house Louis Vuitton (founded in 1854) with Moët Hennessy, which had been established by the 1971 merger of champagne producer Moët & Chandon (founded in 1743) and cognac producer Hennessy (founded in 1765). Bernard Arnault has led the Group since 1989 and is the majority shareholder, pursuing a clearly focused vision. Under his leadership, LVMH has grown to become the world's largest luxury goods conglomerate.

2. Industry & Market Analysis

The luxury goods market has been on a roller coaster journey over the past few years. During the pre Covid period, the luxury market was on a steady growth trajectory, driven by rising global wealth, international tourism and strong demand from Chinese consumers. After Covid struck, it's not surprising the luxury market took a dive due to travel restrictions and economic uncertainty. There was a strong rebound post Covid when countries opened up their borders and lives returned to normality. But in 2025, after years of robust post pandemic growth, it is starting to slow down again. The demand for luxury goods from key markets, especially China is also weakening.

There seems to be a huge shift in China’s consumer patterns as economic uncertainty looms and erodes consumer confidence. The recent fall out in the Chinese property market didn't help matters either. Chinese consumers are now more cautious on high ticket luxury items and there are also signs that consumers are now prioritizing experiences over material goods, especially among the younger consumers.

In 2025, the industry faces a pivotal shift as growth decelerates, and businesses adjust to evolving consumer demands, technological advancements, and economic challenges. The post-pandemic landscape is defined by a more measured and sustainable approach to expansion, an increasing emphasis on digital and experiential luxury, and emerging global opportunities. As China’s leading position comes under scrutiny, new markets like India gain prominence. Despite facing volatile macroeconomic conditions and shifting consumer trends, the group’s diversified portfolio and global presence have enabled it to maintain its leadership in the luxury sector.

3. Business Model & Strategy

LVMH is the undisputed market leader in the luxury space with 75+ prestigious brands across wines & spirits, fashion & leather goods, perfumes & cosmetics, watches & jewelry, and selective retailing under its belt. Each brand operates with significant autonomy while benefiting from group resources and there is also strong emphasis on product quality, craftsmanship, and innovation across all its brands.

Its diverse portfolio prevents it from being overly reliant on any single brand or segment and its market leadership gives it a huge competitive advantage with premium pricing power, high margins, and a robust global distribution network.

2025 has been a challenging year so far and the company is proactively taking steps to ride out the head winds and stay ahead of its competitors. LVMH is shifting its core strategy toward ultra-affluent customers, positioning luxury as an everyday experience for the elite rather than an occasional treat for aspirational buyers. To reduce exposure to geopolitical risks and tariff challenges, LVMH is restructuring its supply chain by expanding regional operations, broadening its network of suppliers, and relocating production closer to key markets. This strategy strengthens the company against trade uncertainties and currency fluctuations. Additionally, expanding into stable regions like Europe and fast-growing economies provides further protection against localized economic downturns.

4. Financial Analysis

Over the past five years, LVMH has consistently expanded its revenue base, with notable growth following the pandemic-affected year of 2020. The group’s performance peaked in 2023, before moderating in 2024 amid global economic headwinds and currency fluctuations.

Revenue Growth:

LVMH’s revenue rose from €79.2 billion in 2022 to a record €86.2 billion in 2023, before easing to €84.7 billion in 2024. This trajectory reflects both the group’s recovery from the pandemic and the impact of softer luxury demand in key markets in 2024.

Profitability:

Operating profit climbed from €21.1 billion in 2022 to €22.8 billion in 2023, then declined to €19.6 billion in 2024. The operating margin contracted from 26.5% in 2023 to 23.1% in 2024, reflecting increased cost pressures and less favorable market conditions.

Net Profit:

Net profit reached €15.95 billion in 2023, before falling to €12.96 billion in 2024, mirroring trends in revenue and operating profit.

Business Segments:

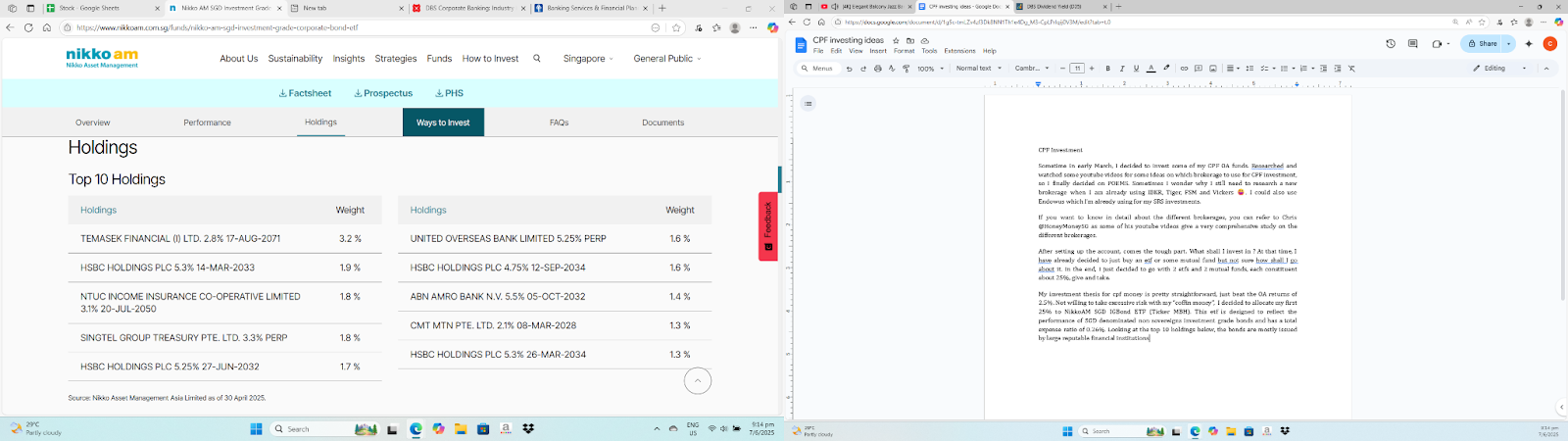

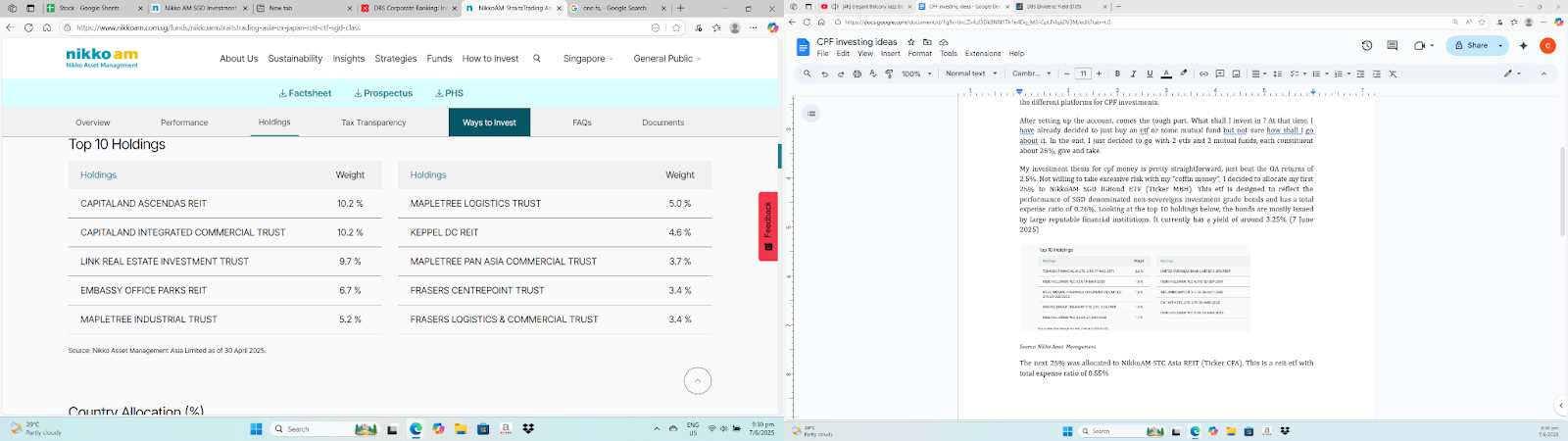

Fashion & Leather Goods continued to be the group’s powerhouse, contributing the largest share of revenue and profit. However, this segment, along with Wines & Spirits and Watches & Jewelry, experienced declines in 2024. The Selective Retailing segment, which includes Sephora, remained resilient and stable.

For FY2024, LVMH reported revenue of €84.7 billion, down 2% year-on-year. Profit from recurring operations was €19.6 billion, a 14% decrease from 2023. Net profit attributable to the group was €12.6 billion. Despite the revenue and profit declines, free cash flow increased by 29% to €10.5 billion, underscoring the group’s strong cash generation.

Growth was mainly driven by Europe, the United States, and Japan, while performance in Asia was mixed due to evolving Chinese consumer behavior. Currency headwinds, particularly the strong euro, negatively impacted reported results, especially in the Fashion & Leather Goods and Wines & Spirits segments.

In its latest Q1 2025 results, LVMH posted revenue of €20.3 billion for the first quarter of 2025, down 2% year-on-year (down 3% on an organic basis). Europe showed continued growth at constant scope and currency, while the United States saw a slight decline. Japan remained stable, and the rest of Asia was flat or slightly down, reflecting a normalization in Chinese demand after a period of strong growth.

Segment performance for Q1 2025:

Fashion & Leather Goods: €10.1 billion (down 4% YoY)

Perfumes & Cosmetics: €2.18 billion (flat YoY)

Watches & Jewelry: €2.48 billion (up 1% YoY)

Wines & Spirits: €1.3 billion (down 8% YoY)

Selective Retailing: €4.19 billion (flat YoY)

The table below compares key metrics between LVMH and its peers, highlighting why LVMH stock has underperformed. While I wouldn’t say the company is in dire straits, it has certainly hit a roadblock. To regain momentum, LVMH must explore new avenues for growth—otherwise, it risks falling behind Hermès and Richemont.

Source: Seeking Alpha

5. Risks & Challenges

With China’s economy slowing and Chinese consumers becoming more selective with their spending, LVMH must seek new markets to sustain revenue growth. However, if a global recession is triggered by ongoing trade tensions, this strategy could be disrupted. Additionally, LVMH faces fierce competition from Hermès, which has pursued a different approach to growth. As of April 2025, Hermès has overtaken LVMH as the world’s most valuable luxury company by market capitalization, focusing on an ultra-high-net-worth clientele. This strategy makes Hermès less vulnerable to economic downturns that affect aspirational and middle-class luxury buyers.

6. Conclusion

Although LVMH stock has underperformed, I still believe its business fundamentals remain strong. I have dollar-cost averaged within the €450 to €600 range, maintaining confidence in the company’s long-term prospects. Additionally, I have also initiated a position in Hermès, though the stock is currently somewhat overpriced. If there are dips in the share price, I plan to add more Hermès shares to my portfolio also.